05.07.2024

The challenge for crypto industry actors and regulators is to navigate unknown waters and find a common understanding to protect market interest without sacrificing technological innovation.

Maximal Extractable Value (MEV) has become a controversial technological aspect within the crypto industry, blockchain, and especially the growing world of DeFi (Decentralized Finance). With the implementation of the Markets in Crypto Assets (MiCA) regulation by European authorities, which aims to establish a legal framework for technical innovations in crypto assets, MEV has come under scrutiny. According to MiCA guidelines, MEV is considered an abusive market practice and, therefore, illegal.

Understanding MEV.

MEV is the potential value miners or validators can extract from reordering, excluding, or including transactions within a block. MEV is mainly extracted using two techniques: front-running and sandwich attacks. In the first case, the miner or validator places their transaction ahead of others to capitalize on a favorable price fluctuation; in the second case, they place two transactions around a target transaction to exploit price swings.

MEV extraction by front-running is mostly practiced by “searchers” and not by validators; they use algorithms to detect arbitrage opportunities and bots to execute the transactions once identified. The opportunity resides in making a transaction ahead of another user and capitalizing on the order of transactions on the mempool. The validator profits from the gas fees paid by the searcher, who will pay the highest bet for their transactions being included in the block.

On the other hand, MEV extraction by sandwich attacks is often interpreted as a malicious activity because of its potential for market and price manipulation. Let’s say a user places a buy order in a DEX (decentralized exchange), then an MEV bot exploits the trade by placing two orders, one to increase the token price before the order execution and an order to sell the token at an inflated price. The amount the user finally pays depends on the “slippage”; thus, the price difference the user is willing to accept between the trade order and the final price execution.

MEV’s Role in DeFi Ecosystems and DEX Arbitrage.

MEV supporters argued that this mechanism is crucial to the efficiency of the DeFi ecosystem, for instance, in improving the allocation of blockspace. Automated Market Makers (AMMs) in DEXs like Uniswap rely on liquidity pools, in which the trades are not matched by order books (like in a centralized exchange that has the custody of the assets) but instead on pooled assets by users. The MEV techniques create arbitrage opportunities, which in turn help maintain the balance of liquidity pools, thereby contributing to market stability.

Regulatory Concerns and MiCA

The European Union, though the MiCA (Markets in Crypto-Assets Regulation) implementation, has made a controversial stand-off against MEV, marking it as an illegal market abuse. The European Securities and Markets Authority (ESMA) has stated: “...MiCA is clear when indicating that orders, transactions, and other aspects of the distributed ledger technology may suggest the existence of market abuse, e.g., the well-known Maximum Extractable Value (MEV) whereby a miner/validator can take advantage of its ability to arbitrarily reorder transactions to front-run a specific transaction(s) and therefore make a profit.”

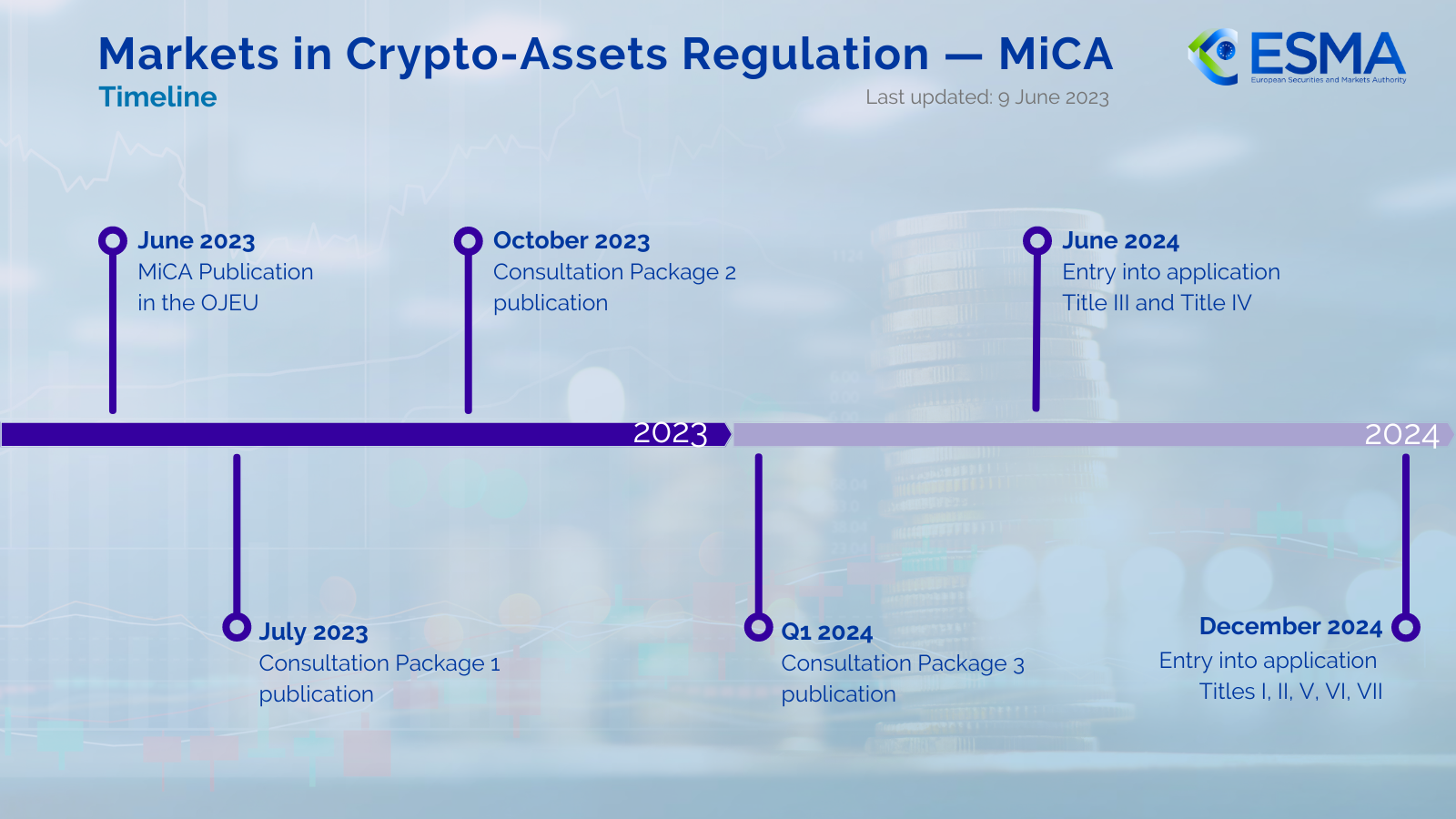

Source: MiCA Timeline

{kind=link}

This MEV categorization has raised alarms across the crypto industry, as ESMA’s and MiCA’s approach is considered a misinterpretation of blockchain dynamics. A crypto player such as Paradigm argues that, unlike traditional markets, blockchain transactions are public and transparent. In contrast, in regulated markets, front-running implies using confidential information and data to gain an unfair advantage. All participants in the blockchain can see the transactions, which Paradigm asserts nullifies the traditional concept of front-running in this context.

While protecting users' and investors' interests against potential abuses and market manipulations is commendable, these measures must be balanced with the innovative drive that blockchain and the crypto asset market offer through their technology. Regulators must consider that, in many cases, interpreting the dynamics of blockchain requires an unconventional approach and a legal framework that cannot be identical to traditional markets.